Article Brief

Why this article matters

US AI investment is happening at a scale never seen before (285.9 billion private dollars in 2025, 725 billion in hyperscaler capex in 2026), and yet the quality gap with Chinese models collapsed to 2.7%. With inference prices 10 to 100 times lower, companies like Coinbase, Airbnb, and Cursor have already moved real workloads to GLM, Kimi, Qwen, and DeepSeek. In this post I break down the numbers from both sides, analyze the risk to Western infrastructure, review the security implications (that almost nobody is looking at), and explain why I think the market is heading toward a dual model: Western frontier models for the complex and critical work, cheap Chinese models for everything token-hungry and repetitive-agentic.

If China Matches the US With 23x Less Money... What Are We Actually Paying For?

On Friday, June 26, 2026, Brian Armstrong (CEO of Coinbase, the largest regulated crypto exchange in the United States) posted on X something that ruined more than one person's weekend. He said Coinbase had been experimenting with setting open-weight Chinese models, GLM 5.2 from Zhipu and Kimi K2.7 from Moonshot, as the default in their internal LLM gateway. The result, in his own words: "Putting this into practice has cut our AI spend nearly in half, while our token usage continues to grow." AI spend dropped almost by half. Token consumption kept growing. And 91% of their engineers didn't even notice the difference, because they never hit the old usage limits anyway.

A publicly traded, super-technical, regulated US company in the financial sector, moving the bulk of its internal AI workloads to Chinese models. Not some cash-strapped startup burning runway, COINBASE!

When I read that it clicked hard, because I'd been chewing on this idea for weeks, and I'd even been talking about it constantly with a coworker. So I did what any of us would do in 2026: I put several models to work researching the topic in parallel, American and Chinese ones. ChatGPT, Gemini, Perplexity, Grok on one side... DeepSeek, Kimi (it did an excellent job), and Qwen on the other. Several 'deep research' reports on the exact same questions (the same prompt). And here's the part that struck me as almost poetic: the reports from the Chinese models, researching their own disruption, cost me cents. The Western ones cost several dollars. The thesis of the article was proving itself while I was still in the first stage of researching it.

This led me to a video from a YouTube channel I love, one that's usually focused on personal finance and investing, the excellent channel by Andrei Jikh, with his signature super clear and polished videos... Not coincidentally, his latest video titled "China Is About To Pop The AI Bubble" covers exactly this, and even talks about the famous distillation attack.

Andrei Jikh's video connecting the AI financial bubble to the pressure from Chinese models

This post is the result of that work: mixing AI-driven and manual research, the video, everything we kept discussing with my peers and, above all, the hard numbers on investment, the evidence that the quality gap has practically closed by now, the real migration cases, the security angle that almost nobody is discussing seriously, and my personal read on where all of this might be heading. Spoiler alert: I don't think anyone wins by knockout, I think the market is going to end up splitting in two, using the best of both worlds.

The Paradox: 23 Times More Resources for Under 3% of a Difference

Let's start with the number that kills the narrative. According to the 2026 AI Index Report from Stanford HAI, private AI investment during 2025 reached $285.9 billion in the United States versus $12.4 billion in China. A 23-to-1 ratio. In 2024 that ratio had been 12-to-1 ($109.1 billion versus $9.3 billion). California alone attracted $218 billion, more than the rest of the planet combined.

With that capital asymmetry, plus four rounds of chip export controls specifically designed to choke off Chinese access to frontier GPUs, you'd expect a proportional quality gap, right? Well... it didn't happen, or rather, it happened for a brief window of time.

The same report documents that the performance gap between the best US and Chinese models went from 17.5 to 31.6 percentage points in May 2023 to a 2.7% gap in March 2026. In the LMArena Elo ranking, Claude Opus 4.6 led with 1,503 points against ByteDance's Dola-Seed-2.0's 1,464. That's 39 Elo points. A margin that could flip with any newer release of models like Opus 4.8 or GLM v5.2. These "old" models get compared because they're the ones that appear in the report cited from March, but the reality is that today that gap is even smaller.

To back this up with something beyond my own claim, here's the real ranking from the Artificial Analysis Intelligence Index, one of the industry's most cited independent indexes for measuring aggregate capability across models. Notice where the Chinese models land: not at the bottom of the table like in 2023, but interspersed at the top of the pack alongside the Western ones.

Artificial Analysis Intelligence Index, independent capability ranking across models (July 2026)

Independent comparison of GLM 5.2 vs Claude Opus 4.8, by Michael Tefula

You can find more on all of this in the following links:

- https://www.braintrust.dev/blog/glm-52-vs-opus-48-long-context-retrieval

- https://www.michaeltefula.com/blog/glm-5-2-vs-opus-4-8/

- https://openrouter.ai/compare/z-ai/glm-5.2/anthropic/claude-opus-4.8 (clearer and more concise, less text)

Two important clarifications to keep this honest, because this is exactly where most hot takes fall apart:

First, the Chinese investment figure is understated. Stanford's own report says so: Chinese government guidance funds deployed roughly $912 billion into strategic industries between 2000 and 2023, with about $184 billion directed at AI companies, and in 2025 Beijing announced a state-backed venture capital fund of $138 billion over 20 years for AI and quantum computing. The "private vs. private" comparison favors the American narrative more than reality justifies.

Second, parity isn't total. On the most specialized and demanding benchmarks (doctoral-level scientific reasoning like GPQA Diamond, long-horizon agentic orchestration, heavy tool use, etc.) Western frontier models keep a real advantage of between 5 and 10 points, and analyses like Brookings' and CAISI's estimate the Chinese frontier runs 6 to 9 months behind. The gap exists, it's a reality. But here's the other side of it: the reality is that for 90% of the tasks a company runs every single day, that gap is irrelevant.

The investment-quality paradox between the US and China

The Bottom Line

Some numbers here are a little stunning: China now leads in the sheer volume of AI scientific output, with 23.2% of global publications, 20.6% of research citations (versus 12.6% for the US), and nearly 70% of the world's AI patent filings. The narrative that America's advantage is structural and unassailable has stopped being backed by the data.

How They Did It: Efficiency by Design (and a Controversy)

The obvious question is how. How an ecosystem with 23 times less private capital and no access to the best chips got close enough to fight for the frontier. The answer has three parts, and they're worth understanding because they explain why the cost advantage isn't a marketing trick but something structural.

1. Sanctions as a catalyst

US export controls forced Chinese labs to do more with less. DeepSeek trained its V3 model on a cluster of 2,048 H800 GPUs (the degraded version NVIDIA built to comply with the restrictions) at a declared pre-training cost of $5.6 million, versus the more than $100 million estimated for GPT-4. On January 27, 2025, once the market processed what that meant, NVIDIA lost $589 billion in market cap in a single day, the largest one-day loss in stock market history. The famous "DeepSeek moment."

Be careful with that $5.6 million figure, which got repeated endlessly without context. SemiAnalysis estimates DeepSeek spent over $500 million on GPUs across its history, and the declared number excludes all the prior research and failed experiments, so a direct comparison to Western training costs can be pretty misleading. Even accounting for that correction, though, the order-of-magnitude difference in efficiency is real.

2. Mixture-of-Experts architectures pushed to the extreme

Here's the technical heart of the matter. The latest generation of Chinese models are giants in total parameters but dwarfs in active parameters. DeepSeek V4 has 1.6 trillion total parameters but activates between 37 and 49 billion per token. Kimi K2 has over 1 trillion and activates around 32 billion. On top of that, they added radical KV cache compression: the V4-Flash variant uses just 7% of the cache and 10% of the FLOPs of the previous generation. The result is that serving inference costs them a tiny fraction of what it costs a dense model of comparable quality.

3. Open-source as a strategic weapon

And the masterstroke ended up being... publishing the weights. Alibaba's Qwen surpassed 700 million downloads on Hugging Face in January 2026, overtaking Meta's Llama (for the first time). DeepSeek, GLM, and Kimi are distributed under MIT or similar licenses. This has two brutal effects:

- It enables self-hosting (meaning near-zero variable cost beyond your own infrastructure).

- It makes regulatory blocking nearly impossible, because you can't sanction a model that runs locally and is already downloaded across half the world.

The Distillation Controversy

Here's the uncomfortable part of the story. OpenAI and Google accused DeepSeek of training its models by distilling outputs from their own models through their API, and in 2026 Anthropic testified before Congress denouncing what it described as the largest known distillation attack (self-referenced). More than 28.8 million interactions extracted from Claude through a network of roughly 25,000 fake accounts, attributed to the Qwen group but with suspected cooperation from other Chinese AI labs like DeepSeek and Moonshot (Kimi). The White House called it industrial-scale distillation, while the Chinese labs flatly denied it.

So there's a belief that part of China's efficiency is indirectly subsidized by Silicon Valley's multi-billion-dollar R&D, in a dynamic that's parasitic in the best sense of the word... and undeniably effective (we mere mortals should probably be grateful) where chip controls attack access to frontier hardware, but where algorithmic knowledge mixed with heavy compute leaks straight out through the API.

Think of the famous distillation attack as two glass vessels connected by thousands of tiny, almost invisible tubes. On one side, the enormous vessel, filled over years with concentrated knowledge at the cost of hundreds of millions of dollars in training. On the other, a much smaller vessel that fills drop by drop with that same essence, except each drop comes out more condensed and cheaper than the last. No direct attack, no classic exploit. Just thousands of queries disguised as normal traffic, slowly draining the intelligence and value out of that big vessel.

Knowledge distillation between AI models, the signature attack of the new tech race

The 'Cold' Price War and the Numbers That Matter

Everything above was just context. Now let's actually look at what hits your bill (API prices per million tokens as of mid-2026). These will surely have changed by the time you're reading this, but the important part here is the order of magnitude:

| Model (origin) | Input / 1M tokens | Output / 1M tokens |

|---|---|---|

| GPT-5.5 (OpenAI, USA) | $5.00 | $30.00 |

| Claude Opus 4.8 (Anthropic, USA) | $5.00 | $25.00 |

| Gemini 3.1 Pro (Google, USA) | $2.00 | $12.00 |

| GLM 5.2 (Zhipu, China) | $1.40 | $4.40 |

| Kimi K2.7 (Moonshot, China) | ≈$0.60 | ≈$2.50 |

| DeepSeek V4 Pro (DeepSeek, China) | $0.43 | $0.87 |

| DeepSeek V4 Flash (DeepSeek, China) | $0.14 | $0.28 |

It's wild, and worth reading twice... on output, between GPT-5.5 and DeepSeek V4 Flash there's a difference of more than 100 times, and that's not even the floor, because with aggressive caching DeepSeek charges cache hits at $0.028 per million. Justin Summerville, from OpenRouter, summed it up for CNBC: open Chinese models are consistently 60% to 90% cheaper than the best offerings from Anthropic and OpenAI.

But the comparison I liked the most out of the whole research is Armstrong's own, because it's a real enterprise workload, not list prices or some abstract comparison table:

- The same workload on Claude: $4,811

- On GPT-5.5: $3,357

- On DeepSeek V4: $1,071

- On Kimi K2.7: $948

- On GLM 5.2: $544

Same task, a nearly 9x smaller bill between the extremes. When your agents and multi-agent systems are burning through billions of tokens a month, that stops being a line item in your budget and becomes THE budget.

The collapse in the price of intelligence

But Why Did This Blow Up Right Now? The Agents

There's a structural detail that explains the timing, and it's the key to this whole phenomenon, in my view. LLM usage stopped being chat and became agentic, I wish I could say it was a gradual shift, but it really wasn't, and today just about any moderately technical person is already building their own agents for their own workflows (not to mention at the company level).

On OpenRouter, agentic coding and programming workloads went from about 11% of traffic in early 2025 to more than 50% by mid-2026. But... what actually is an agent?

An agent, in short, doesn't just generate a response (like an LLM does), it also generates chains of reasoning, tool calls, retries, corrections, entire loops of work that are more or less complex depending on the LLM running underneath. To put it more clearly: it's an LLM (the brain) inside a full body, where arms and legs give it abilities, eyes let it see with more precision, ears let it perceive the environment, and so on. This ended up changing token consumption per task, multiplying it exponentially depending on how complex the workflow is.

Once the price per token gets multiplied by agentic volume... elasticity shows up on its own. Gartner already predicted that by 2028 AI coding costs will exceed the average software developer's salary. Uber burned its entire 2026 AI budget in four months. At Lindy, an agent startup, inference costs exceeded the company's entire payroll. That's the context in which a model that's 10 times cheaper with 97% of the quality stops being a curiosity and becomes a survival decision.

The Migration That's Already Happening

The timeline of the last year and a half:

The DeepSeek Moment

DeepSeek releases its V3/R1 models, trained at a fraction of the Western cost. NVIDIA loses $589 billion in market cap in a single day. The premise "more capital = better AI" takes its first public hit, and mainstream (non-specialized) media picks up the story.

Airbnb Picks Qwen

Airbnb CEO Brian Chesky admits his company relies heavily on Qwen (Alibaba's model) in production because it's "really good, fast, and cheap." Its customer service agent runs on 13 models and cut resolution time from nearly 3 hours to 6 seconds.

OpenRouter: The Crossover

Starting February 8th, Chinese-origin models exceed 30% of weekly token volume on OpenRouter every single week, with peaks of 46%. A year earlier they were under 5%.

The USCC's Two Loops Report

The US-China Economic and Security Review Commission warns that the proliferation of open Chinese models creates "alternative paths to AI leadership." It cites the estimate from Martin Casado, general partner at the venture capital fund Andreessen Horowitz (a16z), one of Silicon Valley's most influential funds, saying that roughly 80% of the AI startups pitching his fund are already running on Chinese open-source stacks.

Congress Investigates

The Homeland Security committees and the Select Committee on China send formal letters to Airbnb and Anysphere (Cursor) demanding explanations about their use of Chinese models. Cursor had built Composer 2, its flagship feature, on top of Moonshot's Kimi K2.5.

The Coinbase Effect

Armstrong announces a 50% cut in AI spend by defaulting to self-hosted GLM 5.2 and Kimi K2.7. Lindy migrates 100% of its Claude traffic to DeepSeek V4. Anthropic and OpenAI respond with aggressive price cuts.

A few details that feel important before buying the whole narrative, because sensationalist viral data almost always needs a caveat or a deeper look:

- The "80% of startups" figure is Casado's observation about the pitch decks he sees at his own fund, cited by the USCC in its Two Loops report. It's not a systematic, comprehensive industry survey.

- On the other hand, OpenRouter's shares measure token volume, not revenue. Anthropic and Google still capture the premium revenue, and the Anthropic-OpenAI duopoly (plus Google) still concentrates around 90% of enterprise AI spend. There's actually a beautiful data point that sums up the whole asymmetry, from a routing analysis: 42% of revenue came from just 11% of tokens. The premium tier charges a lot and processes little, while the commodity tier processes everything and charges cents.

But the direction here is clear... and on the other side of the board, Western financial exposure is enormous. The four hyperscalers are planning a combined capex of ≈$725 billion in 2026 (a 77% jump year-over-year), OpenAI has accumulated infrastructure commitments of $1.4 trillion against annualized revenue of ≈$20 billion, and Sequoia Capital calculates that the industry needs about $600 billion in annual revenue to justify current spending... while, for better or worse, actual revenue sits around $100 billion.

If the model layer gets commoditized (which is exactly what Chinese pricing is forcing), part of that infrastructure turns into what analysts call a stranded asset (basically an asset that never recovers its investment value), with an aggravating factor compared to previous bubbles that few people notice: back in the 90s, fiber optic cable installed at scale across the US lasted 20 years; today, a GPU's compute power depreciates in roughly 1 to 3 years.

Again, this isn't some conceptual illustration of mine or an unfounded opinion, this is the real map of the capex hyperscalers have already committed to for 2026, compared against Chinese spending in the same race. The investment asymmetry from the section above, scaled up to the physical infrastructure being built right now.

The 2026 AI capex war, in real numbers

The Security Angle: What Almost Nobody Is Looking At

Here's where I put on my professional hat, because within this whole cost debate there's a security layer that's barely being discussed, where the focus always ends up being more about geopolitics and investment than engineering. Let's separate the real problems from the slogans:

Data residency as a major problem

If you use the DeepSeek or Moonshot API directly, your prompts and outputs travel to servers subject to Chinese cybersecurity law. For any company processing personal data under GDPR, financial data, or customer PII, that's a de facto blocker. Unfortunately, this isn't paranoia, it's basic compliance. That's why DeepSeek was banned at NASA, the US Navy, the Pentagon, and several states (for that reason, and for geopolitical ones too).

Self-hosting as a partial solution.

- This is where the decisive technical nuance gets skipped in the public discussion. Open models can be downloaded and served on your own infrastructure (with vLLM or any inference server), which keeps prompts and outputs on infrastructure you control and completely eliminates cross-border data flow. Coinbase did exactly that, ultimately downloading GLM and Kimi's open-source models onto its own servers so neither the code nor the queries ever touch endpoints in China. An October 2025 evaluation from the Center for AI Standards and Innovation (CAISI) confirms that local deployment solves the data residency and exfiltration problem.

What self-hosting does NOT solve.

- As a central point for anyone working in security or AI security: bias, censorship, and susceptibility to jailbreaks are properties of the weights, not of where the model is hosted. You can run it in your own datacenter in Buenos Aires, Asunción, São Paulo, wherever, and the model still carries whatever it was built with at the factory (how it was trained). NIST evaluated in September 2025 that agents built on DeepSeek's most secure model were, on average, 12 times more likely to follow malicious instructions than agents based on US frontier models.

- For an internal FAQ chatbot, maybe you don't care.

- For a complex customer-facing chatbot, maybe you should care a bit more.

- For an agent with tool access, write permissions, and production data, it's a massive difference in threat model.

This is my favorite image in the whole post for explaining this to someone just starting out in AI security: think of it as a transparent, armored glass vault that perfectly blocks everything trying to get out. Inside, the entire model, its efficient intelligence, downloaded and running. The problem is the dark pattern isn't outside trying to get in, it's already declared inside the weight network, inside the vault, where no guardrail is going to filter it because it doesn't recognize it as an external threat. A guardrail can block direct and indirect prompts, and can even return the model's output to the user, but the reality is that if the model is weak by design, even the best guardrail in the world is going to struggle to protect the user from an attack.

The limits of self-hosting as a security control

My Checklist for Adopting Chinese Models Seriously

- Never the direct API for sensitive data: self-host it, or use a Western inference provider with Zero Data Retention (Together, Fireworks, Groq, Baseten, even AWS offers Chinese models now).

- Guardrails in front of and behind the cheap model: susceptibility to malicious instructions gets mitigated with layers, not trust.

- Apply model provenance to your risk framework or evaluation: where the weights come from, who trained them, and on what data is now a supply chain question, the same logic we already apply to software dependencies.

- Keep frontier models for orchestration and decision-making tasks: a weak planner propagates malformed inputs to every downstream agent with no correction mechanism, which is why complex tooling like OpenClaw, NemoClaw, etc. paired with small local models can be like handing a monkey a knife, it might turn out fine, or it might turn out very much not fine.

And one regulatory irony to close this section... while Washington investigates Airbnb and Cursor for using Chinese models, the US government forced the commercial suspension of two Anthropic frontier models for foreign users in June 2026 over national security concerns (Fable 5 and Mythos), citing national security concerns, a move that ended up pushing European partners as well, who consequently fell right into Chinese alternatives, which, being open-weight, can't be remotely "switched off." France fired Palantir days later; Germany and Spain had already been distancing themselves, and today Spain has told them the same thing. The lesson the world learned is uncomfortable for both sides: the only AI nobody can cut you off from is the one running on your own servers.

The Two Scenarios (and Why I Think Neither One Wins)

All the evidence above feeds two opposing narratives, so let's lay them out honestly.

- Scenario A, the West keeps the throne.

- The arguments are solid: real leadership at the frontier (on the toughest reasoning and long-horizon agentic benchmarks, the edge persists), trust, compliance, SLAs, ecosystems integrated with Azure, Google Cloud, and AWS, and an enterprise lock-in that a pricing table doesn't break. For regulated finance, healthcare, defense, and any vertical where a mistake carries legal cost, the Western premium gets paid without question. Dario Amodei (CEO of Anthropic) also argues that Chinese models are overoptimized for benchmarks, and that raw capability, not price, determines long-term adoption.

- Scenario B, commoditization devastates the American model.

- If 80% of volume migrates to models that are 99% cheaper (Armstrong's literal prediction for the next 12 to 18 months), the revenue that justifies Western valuations and capex never materializes. Model-layer margins collapse, the next training generation (projected at $10 to $100 billion) loses its business case, and a meaningful chunk of the $725 billion in 2026 capex ends up as idle capacity depreciating at GPU speed... bubble much?

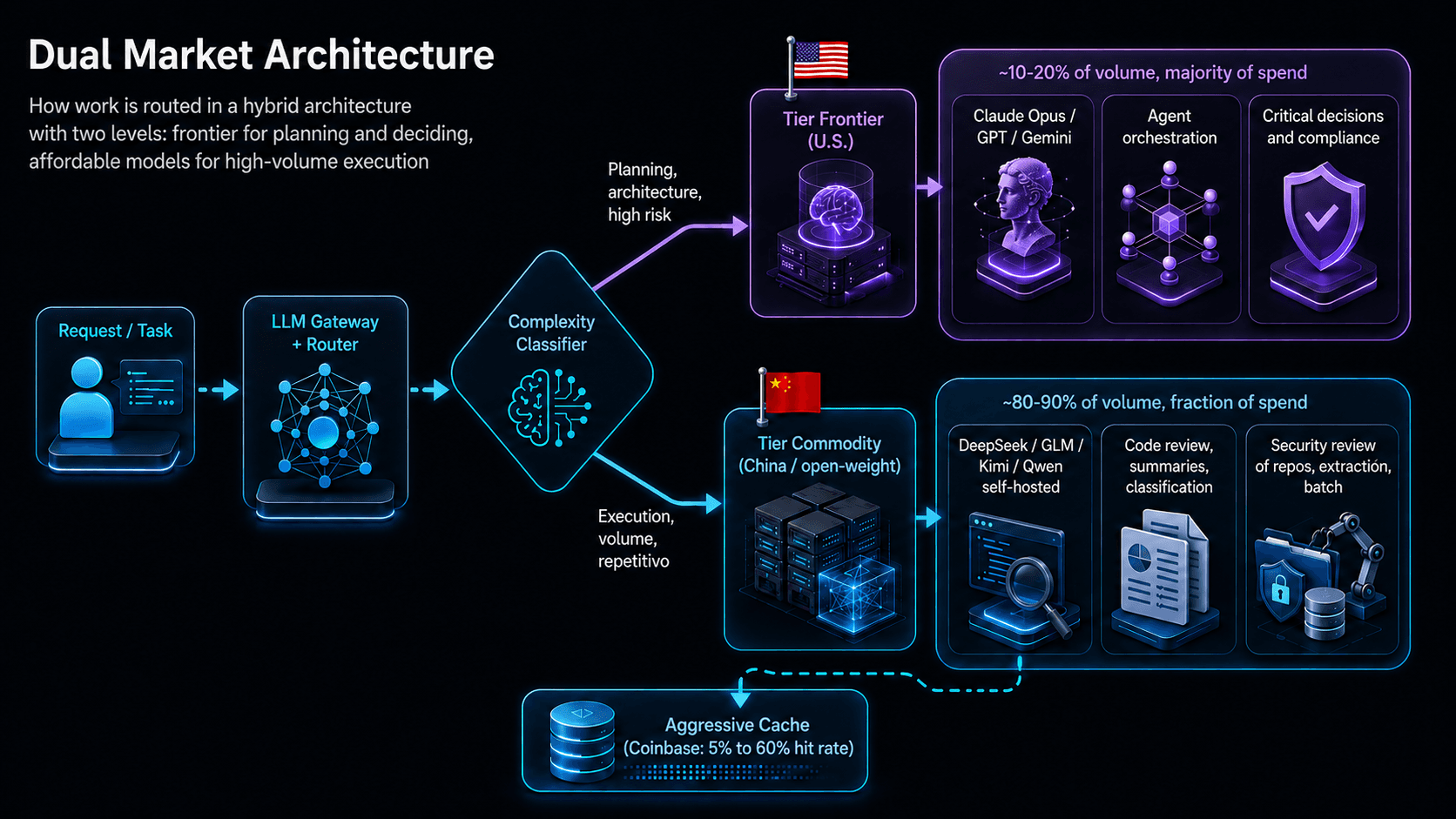

My read, and here's the thesis I've been holding onto for a while now: the market is moving, slowly at first, toward a dual model. This isn't some diplomatic tie, it's the logical consequence of how work actually gets distributed in real agentic systems.

Look at how token consumption breaks down in any serious agentic pipeline. On one hand, planning and architecture decisions are a tiny fraction of the volume, and on the other, execution (writing code, reviewing diffs, summarizing documents, classifying, extracting, iterating) is the overwhelming majority. So the natural split should look something like this:

- Western flagship models (Claude, GPT, Gemini) for the specific and complex work, like architectural planning, agent orchestration, long-chain reasoning, high-risk decisions where a 5% error propagates through the whole pipeline, and anything touching hard compliance.

- Powerful, cheap Chinese models for what's token-hungry, meaning execution-heavy agentic workflows, concrete task-based programming, mass code review, summarization, classification, and cases like a full security review of a repository, where you literally have to feed hundreds of thousands of lines of code through the context and cost per token IS the design variable.

That last example isn't random. In my world, running a security analysis on a large monorepo with a model at $25 per million output tokens is a project with its own budget, and one that raises questions like: which team has to absorb the cost of this security scan? AppSec? Engineering? Where should the money come from? Should it come from the personal inference budget of that repo's owner? A dedicated API key for just that scan or that project? And several other equally entertaining and hard-to-answer questions once you're inside a corporation. Running the same scan with a model at $0.87, on the other hand, is a cron job. The price difference doesn't change the margin... it directly changes what's possible.

The quantitative evidence backs this up, since difficulty-based routing can cut costs by 50% to 70% with no drop in final quality, precisely because execution dominates the volume. That's exactly what Coinbase implemented, it's what Vercel reported when it saw GLM 5.2 adoption multiply its daily token volume by 27x in a single week ("price is doing all the work here," said its head of agentic infrastructure), and it's what Gartner formally recommends as model routing.

So who wins in that world? My conclusion, which I find less obvious and more important, is that the value layer migrates to the router. If the cheap model handles the volume and the expensive model handles the criticality, whoever controls the routing decision controls the costs of the entire chain. And in fact, Armstrong himself said as much: "The layer that can efficiently route each workload to the right model becomes increasingly valuable. Western labs aren't going to go bankrupt, but they're going to have to abandon the paradigm of charging a premium on every single token indiscriminately, and the hyperscalers are going to fight to be the neutral layer that hosts everyone, no matter who wins."

AI's dual market: my central thesis

What I'd Do Today (Practical Guide)

If you manage AI spend at your company or on your projects, here's what the evidence suggests, in order:

Before the steps, here's the mental image that helps me design any of these gateways: a control room seen from above, where a river of heterogeneous requests comes in and a classifier splits them into two channels before they touch a single model. A narrow channel goes to the big, expensive engine. A wide one goes to the army of small, cheap engines. And in the middle, a mirror layer (the cache) that returns the response to some of the requests before they ever reach an engine. That mirror, not the chosen model, is what generates the most savings in practice.

Anatomy of an LLM gateway with difficulty-based routing

- 1

Measure Before Touching Anything

A KPMG study that circulated this year found that only 26% of companies have full visibility into their AI costs, and 22% find out about spend only when the bill arrives. Without telemetry per task and per model, you can't route anything. Coinbase made every developer's spend visible before optimizing.

- 2

Set Up a Gateway With Cheap Defaults

An LLM gateway (LiteLLM, OpenRouter, or your own) with the cheap model as default and frontier models available on demand. The friction to switch is minimal: with OpenAI-API-compatible endpoints, an A/B test is just changing one line for the base URL. The Coinbase pattern: 91% of users don't notice the difference.

- 3

Route by Difficulty, Not by Trend

Frontier for planning, orchestration, and high-risk decisions. Commodity for execution. The practical threshold: if more than 60-70% of your workloads are standardized execution (code review, summarization, classification, extraction), the 10 to 30x savings on those tasks more than pays for the complexity of running multiple models.

- 4

Cache Aggressively

Coinbase's single biggest savings didn't come from switching models: it came from taking the cache hit rate from 5% to 60% through disciplined context engineering (fresh sessions per task, lean histories). The cheapest token is the one that never gets processed.

- 5

Treat Security as a Supply Chain Problem

Self-hosting for sensitive data, guardrails on top of the open weights, model provenance in your risk framework or threat model, and frontier models at the decision points. Everything from the security section above. Price can never be the only variable in the equation.

References

If you want to keep digging into all of this, I recommend:

- Stanford HAI - AI Index Report 2026 - The investment data, performance gap, and scientific output figures.

- CNBC - Chinese AI models gain ground with U.S. companies - The reporting on enterprise migration and the OpenRouter data.

- Brian Armstrong on X - the Coinbase announcement - The original thread with the 50% cut figures.

- USCC - Two Loops: How China's Open AI Strategy Reinforces Its Industrial Dominance - The commission's report on the dual-circulation strategy and the Casado estimate.

- Sequoia Capital - AI's $600B Question - The gap between capex and revenue in the industry.

- CNBC - NVIDIA and the DeepSeek moment (January 2025) - The largest one-day market cap loss in history.

- Fortune - Brian Chesky on Qwen and OpenAI's models - Airbnb in production with Chinese models.

- House Homeland Security Committee - letter to Airbnb - The congressional investigation into Chinese AI usage.

- Yahoo Finance - Chinese AI Models Now Capture Up to 46% of US Token Usage - Weekly OpenRouter data since February 2026.

Closing: Intelligence Is Becoming a Commodity, Judgment Isn't

If I had to sum up this entire research in one idea, it would be this:

- Asymmetric capital bought scale, but it never bought a monopoly on efficiency. The United States spent 23 times more and got a 2.7% edge that rents by the month, not by the year. And on the other side, China turned its restrictions into its competitive advantage (no cutting-edge chips, so it optimized architectures; no premium market, so it slashed prices), and unable to compete on closed models, it opened its weights and worked its way into half the world's infrastructure.

For those of us building with this stuff every day, the takeaway isn't geopolitical, it's architectural. If the cost of basic intelligence trends toward zero, that makes viable things that were unaffordable a year ago (agents running continuously, security reviews of entire repos, pipelines that process everything instead of sampling). But choosing the right model for each task, the routing layer, the guardrails, and the judgment call on when to pay the premium... that doesn't get commoditized. That's where we're going to end up spending our time over the next few years.

If you made it this far, genuinely, thank you for the time. This post took me weeks between cross-referencing research from models on both sides of this war, checking sources, writing, and fixing a few aesthetic components of the blog along the way. The best way to give something back for all that effort is to walk away with one thing: the next time you design a system with LLMs, ask yourselves first which parts of the work actually need the best model in the world... and which parts only need one that's good enough and costs virtually nothing.

Test Your Technical Knowledge

According to Stanford's 2026 AI Index, how did the performance gap between the best US and Chinese models evolve between May 2023 and March 2026?

Coinbase cut its AI spend almost in half while its token consumption kept growing. What combination of levers made that possible?

From a security perspective, why does self-hosting open Chinese weights only solve half of the risk problem?

Continue Reading

Next steps in the archive

Keep Exploring

Related reading

Continue through adjacent topics with the strongest tag overlap.

Compromising Real-World LLM-Integrated Applications with Indirect Prompt Injection

This research introduces Indirect Prompt Injection (IPI), a method to remotely manipulate Large Language Models (LLMs) via malicious prompts in data sources, risking data theft, misinformation, and much more, highlighting the need for stronger defenses.

My First Skills Security Review: OWASP AST10, SkillSpector, and from 60 Findings to 5 Real Ones

It was the first in-house skills security review. The scanner flagged 60 findings across 25 skills. Only about 5 were real, all low impact, all supply-chain shaped. Here is the methodology I ended up using.

The Technical Anatomy of Model Extraction in 2026 (The Great AI Theft of the Century?)

A deep technical dive into Model Extraction attacks. We dissect the mathematics of Knowledge Distillation, logit harvesting pipelines, and the cryptographic failures of LLM watermarking.